Creating a trust is not just about drafting a document; it is about building a legal system for controlling property, protecting beneficiaries, and making sure your wishes can still be carried out if you die or become incapacitated. The practical challenge is that a trust only works when the plan, the paperwork, and the asset transfers all line up.

What a trust is

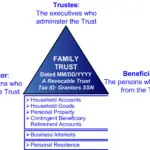

A trust is a legal arrangement in which one person or institution holds property for the benefit of another. The person who creates it is usually the grantor or settlor. The person who manages it is the trustee, and the people who benefit from it are the beneficiaries.

The trust document is the written set of instructions. It says what property belongs to the trust, who controls it, when money or assets are distributed, and what happens if circumstances change. In other words, the document is the blueprint, but the trust becomes useful only when assets are actually placed into it.

Understanding Trusts

Understanding trusts is essential in estate planning and asset management. Trusts can be broadly categorized into two main types: implied trusts and express trusts. Implied trusts are created by the courts based on the conduct and actions of the parties involved, rather than through a written agreement. These trusts are inferred from circumstances, such as when someone holds property for the benefit of another but has not formalized the arrangement. In contrast, express trusts are intentionally established through a written trust document or agreement.

The key distinction lies in the clarity of intent. An express trust leaves no room for ambiguity, as it explicitly outlines the trust’s terms, assets, beneficiaries, and the trustee’s duties. In contrast, implied trusts rely on the understanding of the parties involved and may lack the formality of a written document.

Comprehending this differentiation is crucial, as it affects the enforceability and management of the trust, highlighting the importance of a well-drafted, legally sound trust document in achieving one’s specific goals and ensuring the seamless administration of trust assets.

Why people use trusts

People create trusts for several practical reasons. The most common are avoiding probate, managing assets during incapacity, controlling when beneficiaries receive property, and protecting vulnerable family members. A trust can also reduce delay, keep affairs more private, and create a smoother transition when someone dies.

Trusts are especially useful when heirs are young, financially inexperienced, disabled, or part of a blended family. They can also help where property needs to be managed over time rather than handed over all at once. In that sense, a trust is less about wealth alone and more about control, continuity, and instruction.

Main trust types

The two broad categories are revocable and irrevocable trusts. A revocable trust can usually be changed or canceled during the grantor’s life, which makes it flexible and common in estate planning. An irrevocable trust is much harder to change, but that reduced flexibility is often what gives it stronger protection or special tax or planning advantages.

Other common forms include living trusts, testamentary trusts, special needs trusts, and spendthrift trusts. A living trust is created during life, often to avoid probate. A testamentary trust is created by a will and only begins after death. A special needs trust is designed to support a disabled beneficiary without disrupting certain benefits. A spendthrift trust limits a beneficiary’s direct access to money and can reduce waste or outside claims.

How to establish a trust

A trust should be created in a deliberate sequence rather than as a one-step form filing.

- Define the purpose.

- Choose the trust type.

- Select the trustee and successor trustee.

- Name the beneficiaries.

- Draft the trust document.

- Sign it properly under state law.

- Fund the trust by transferring assets.

- Review it periodically.

The most overlooked step is funding. A trust can be perfectly written and still fail in practice if the assets are never retitled or transferred into it. The document itself does not automatically move property. If you’d prefer my assistance with drafting a trust agreement, purchase my Legal Documentation service.

Choosing the right structure

The right trust depends on the problem you are trying to solve. If you want flexibility and are mainly trying to avoid probate, a revocable living trust is often the most practical option. If you need stronger control over assets or are pursuing more specialized planning, an irrevocable trust may be more appropriate.

For a family with minor children, the trust can set rules for staged distributions. For a homeowner, it can make transfer of the house simpler for heirs. For someone caring for a disabled relative, a special needs trust can provide support while preserving eligibility for important public benefits. For a blended family, the trust can balance the needs of a surviving spouse with the interests of children from a prior relationship.

Trustee and beneficiary roles

The trustee is the person or institution that manages the trust property. That role requires honesty, organization, recordkeeping, and a willingness to follow the trust instructions exactly. A trustee may need to invest assets prudently, pay bills, maintain records, file tax returns, and make distributions on schedule.

The beneficiaries are the people or organizations that receive the benefit of the trust. A trust can give them outright distributions, delayed distributions, or discretionary support for things like education, housing, health care, or maintenance. The more detailed the rules, the less room there is for conflict later.

Naming a successor trustee is also essential. If the first trustee dies, becomes incapacitated, or cannot serve, someone else must be ready to step in without delay. That continuity is one of the main strengths of a well-designed trust.

Funding the trust

Funding means placing assets under the trust’s control. This usually involves changing title or ownership records so the trust is recognized as the legal owner or beneficiary. Without funding, the trust may exist on paper but not actually govern the property you intended it to control.

Common funding methods include a new deed for real estate, transfer forms for bank or brokerage accounts, and coordinated beneficiary designations for assets like retirement accounts or life insurance. Those latter assets are often not retitled directly into a trust, but they still need to be aligned with the overall estate plan. If they are not, they can override or frustrate what the trust is supposed to accomplish.

Common mistakes

The biggest mistake is failing to fund the trust. The second is choosing the wrong trustee, especially someone who is emotionally involved but not capable of handling the responsibility. The third is using a generic form that does not fit the family situation, the asset mix, or the state’s legal requirements.

Another common mistake is forgetting to coordinate the trust with a will, beneficiary forms, powers of attorney, and insurance policies. Estate planning works as a system, not as isolated documents. If one document says one thing and another document says something different, the result can be confusion, delay, or litigation.

Practical use cases

A trust can be useful in very specific situations.

A parent may create a trust so a child receives money gradually rather than all at once at age eighteen or twenty-one. A homeowner may place a house in a trust so the property can transfer more smoothly after death. An older adult may use a revocable trust so a successor trustee can manage finances if incapacity occurs. A person supporting a disabled family member may use a special needs trust so that support can continue without undermining eligibility for services.

Business owners also use trusts to help manage succession and continuity. In blended families, trusts can reduce the risk that assets intended for children are diverted unintentionally. In all of these examples, the trust is doing the same basic job: converting your wishes into a legally enforceable management plan.

What to check before signing

Before finalizing a trust, check whether the goal is clearly stated, whether the trustee is capable, whether the beneficiaries are identified precisely, whether the assets can realistically be transferred, and whether the document fits state law. If any of those parts are weak, the trust may be legally valid but function poorly.

It is also important to think about future changes. Marriage, divorce, death, birth of a child, a move to another state, or a major change in assets can all affect whether the trust still makes sense. Good trust planning is not a one-time event; it is an ongoing process of maintenance and review.

Why the details matter

The strength of a trust lies in alignment. The document, the asset titles, the trustee’s authority, and the beneficiary designations must all support the same plan. When they do, the trust can reduce probate, provide continuity, and protect vulnerable beneficiaries with relatively little friction.

When they do not, the trust becomes an expensive piece of paper. That is why the practical side of trust creation matters just as much as the legal drafting. The real goal is not merely to establish a trust, but to make sure it actually works the way you intended.

It’s highly recommended to read and comprehend Weiss’s Concise Trustee Handbook (see PDF below) to get a firm grasp of the general administration of an Express Trust. Throughout this handbook, a number of useful contracts, agreements and forms are presented as examples for you to build upon. I’ve meticulously transcribed these into editable documents called Trust Management Document Templates. Download them after purchase and simply fill in the blanks or replace the red text with your own information.

It should be noted that once the trust agreement is signed by all relevant parties (Grantor, Trustee and Witnesses / Notary, etc.), it is effectively established and operable unless specific clauses delay its operation. At this stage, the Trustee may apply for an EIN with the Internal Revenue Service (IRS), then use that EIN to open a bank account in the name of the trust. From there, it’s just a matter of properly managing the trust as outlined in the PDF document above.